Key Facts about the Uninsured Population

By Jennifer Tolbert, Patrick Drake and Anthony Damico / December 18, 2023

Throughout the coronavirus the pandemic, the coverage expansions put in place by the Affordable Care Act (ACA), including Medicaid expansion and subsidized Marketplace coverage, served as a safety net for people who lost jobs or faced other economic and coverage disruptions. Building on that foundation, pandemic-era policies, including continuous enrollment for Medicaid enrollees and enhanced Marketplace subsidies, further protected people with low income against coverage losses and improved the affordability of private coverage. As a result, in 2022, the number of nonelderly uninsured individuals continued a downward trend, dropping by nearly 1.9 million from 27.5 million in 2021 to 25.6 million in 2022, and the uninsured rate decreased from 10.2% in 2021 to a record low 9.6% in 2022.

This issue brief describes trends in health coverage in 2022, examines the characteristics of the nonelderly uninsured population, and summarizes the access and financial implications of not having coverage. Using data from the American Community Survey (ACS), this analysis compares health coverage data for 2022 to data for 2019 to report on coverage and trends during the pandemic and also examines changes from 2021 to 2022; because of disruptions in data collection during the pandemic, the Census Bureau did not release 1-year ACS estimates in 2020. The analysis focuses on coverage among nonelderly people since Medicare offers near universal coverage for the elderly, with just 457,000, or less than 1%, of people over age 65 uninsured.

How many people are uninsured?

With the economy rebounding and pandemic-era Medicaid protections and enhanced Marketplace subsides in place, the uninsured rate continued to drop in 2022, driven largely by increases in coverage among nonelderly adults. Coverage gains were larger among nonelderly American Indian and Alaska Native and Hispanic people compared to their White counterparts and among low-income individuals and those in working families versus those at higher incomes and those without a worker in the family.

Both the number of nonelderly uninsured and the uninsured rate among the nonelderly population reached all-time lows in 2022. Following enactment of the ACA, the number of uninsured nonelderly individuals dropped from more than 46.5 million in 2010 to fewer than 26.7 million in 2016, before climbing again prior to the pandemic during the Trump administration. In 2022, there were 25.6 million nonelderly uninsured people, over one million fewer than in 2016.

Key Details:

The uninsured rate dropped in 2022, continuing a downward trend that started during the pandemic. The uninsured rate in 2022 declined to 9.6% from 10.2% in 2021 and 10.9% in 2019, and the number of people who were uninsured decreased by 1.9 million from 2021 to 2022 and 3.3 million from 2019 to 2022 (Figure 1).

Coverage protections put in place during the pandemic drove the decline in the uninsured rate from 2019 to 2022. At the beginning of the pandemic, provisions in the Families First Coronavirus Response Act (FFCRA) required states to keep people enrolled in Medicaid until the month after the end of the COVID-19 public health emergency (PHE) in exchange for enhanced federal funding. Although the Consolidated Appropriations Act, 2023 ended Medicaid continuous enrollment in March 2023, the coverage protections were in effect throughout 2022. In addition, the enhanced ACA Marketplace subsidies first enacted in the American Rescue Plan Act (ARPA) were renewed for another three years in the Inflation Reduction Act of 2022 (IRA). As a result, compared to 2019, the share of nonelderly people covered by Medicaid increased by 1.7 percentage points from 21.0% in 2019 to 22.6% in 2022 and the share of nonelderly people with nongroup coverage increased by 0.5 percentage points from 6.9% in 2019 to 7.5% in 2022. During the same period, employer coverage declined by 0.6 percentage points from 58.1% in 2019 to 57.5% in 2022 (Figure 2).

Compared to 2021, the drop in the number of people without health insurance in 2022 was driven by an increase in employer-sponsored, Medicaid, and non-group coverage among nonelderly adults. After falling during the first two years of the pandemic, the share of people with employer-sponsored insurance increased from 57.0% in 2021 to 57.5% in 2022. While Medicaid coverage rates did not change from 2021 to 2022, the share of people with nongroup coverage increased from 7.3% in 2021 to 7.5% in 2022. (Figure 2).

Administrative data point to larger gains in Medicaid coverage than are estimated by the ACS. According to data from the Centers for Medicare and Medicaid Services (CMS), Medicaid enrollment in December 2022 had increased by nearly 30% since February 2020, with 93 million enrolled compared to 69 million with Medicaid coverage in 2022 reported by the ACS. Some of the discrepancy can be explained by different ways of counting people, but some people may misreport their source of coverage on the survey because they do not know they are covered by Medicaid. In addition, national survey data typically undercount lower income people who are more likely to be covered by Medicaid. While these discrepancies are longstanding, they appear to have doubled during the pandemic.1

Coverage gains were widespread among the nonelderly population during the pandemic but were largest for American Indian and Alaska Native and Hispanic people, individuals in low-income families, and adults. From 2019 to 2022, the uninsured rate for American Indian and Alaska Native people fell 2.4 percentage points (from 21.7% to 19.1%) and the uninsured rate for Hispanic people decreased by 2.0 percentage points (from 20.0% to 18.0%). While the uninsured rate dropped for people at all income levels, individuals in low-income families2 experienced the largest uninsured rate decline from 18.1% in 2019 to 15.7% in 2022. The uninsured rate for nonelderly adults fell 1.4 percentage points from 12.9% in 2019 to 11.3% in 2022 while the uninsured rate for children dropped by less than 0.6 percentage points from 5.6% to 5.1% (Figure 3).

From 2019 to 2022, the uninsured rate dropped in 34 states, including 26 expansion states and 8 non-expansion states; there was not a significant decline in the remaining states. Over the full three-year period 2019-2022, no state saw an increase in the uninsured rate; however, one state, Maine, experienced a statistically significant increase in the uninsured rate from 2021 to 2022. While several non-expansion states experienced large declines in the uninsured rate during the pandemic, the uninsured rate for the group of non-expansion states was nearly twice that of expansion states (14.1% vs. 7.5%) in 2022 (Appendix Table A).

Who is uninsured?

Most of the 25.6 million nonelderly people who are uninsured are adults, in working low-income families, and are people of color. Reflecting geographic variation in income and the availability of public coverage, most uninsured people live in the South or West. In addition, most who are uninsured have been without coverage for long periods of time. (See Appendix Table B for detailed data on characteristics of the uninsured population.)

Key Details:

Of the total nonelderly uninsured population in 2022, nearly three-quarters (73.3%) had at least one full-time worker in their family and an additional 10.9% had a part-time worker in their family (Figure 4). More than eight in ten (80.8%) uninsured people were in families with incomes below 400% FPL in 2022 and nearly half (46.6%) had incomes below 200% FPL. In addition, people of color made up 45.7% of the nonelderly U.S. population but accounted for 62.3% of the total nonelderly uninsured population. Hispanic and White people comprised the largest shares of the nonelderly uninsured population at 40.0% and 37.7%, respectively (Figure 5). Most uninsured individuals (75.6%) were U.S. citizens while 24.4% were noncitizens in 2022. Nearly three-quarters live in the South and West.

Nonelderly adults are more likely to be uninsured than children. The uninsured rate among children was 5.1% in 2022, less than half the rate among nonelderly adults (11.3%), largely due to broader availability of Medicaid and CHIP coverage for children than for adults (Figure 5).

In general, racial and ethnic disparities in coverage persist. The uninsured rates for nonelderly Hispanic (18.0%) and American Indian and Alaska Native people (19.1%) are more than 2.5 times the uninsured rates for White people (6.6%) (Figure 5). However, like in previous years, Asian people have the lowest uninsured rate at 6.0%, although this masks variation in the uninsured rate within the Asian population.

Noncitizens are more likely than citizens to be uninsured. The uninsured rate for recent immigrants, those who have been in the U.S. for less than five years, was 30.3% in 2022, while the uninsured rate for immigrants who have lived in the US for more than five years was 33.1%. By comparison, the uninsured rate for U.S.-born citizens was 7.7% and 9.5% for naturalized citizens in 2022 (Appendix Table B). Separate KFF survey data show how uninsured rates vary by immigration status.

Uninsured rates vary by state and by region; individuals living in non-expansion states are more likely to be uninsured (Figure 6). Ten of the fifteen states with the highest uninsured rates in 2022 were non-expansion states as of that year (Figure 7 and Appendix Table A). Economic conditions, availability of employer-sponsored coverage, and demographics are other factors contributing to variation in uninsured rates across states.

Two-thirds of nonelderly people who were uninsured in 2022 have been without coverage for more than a year.3 People who have been without coverage for long periods may be particularly hard to reach in outreach and enrollment efforts.

Why are people uninsured?

Most of the nonelderly in the U.S. obtain health insurance through an employer, but not all workers are offered employer-sponsored coverage or, if offered, can afford their share of the premiums. Medicaid covers many low-income individuals, especially children, and although the Medicaid continuous enrollment provision led to increases in Medicaid coverage in all states, Medicaid eligibility for adults remains limited in most states that have not adopted the ACA expansion. While subsidies for Marketplace coverage are available for many moderate-income people, few people can afford to purchase private coverage without financial assistance.

Key Details:

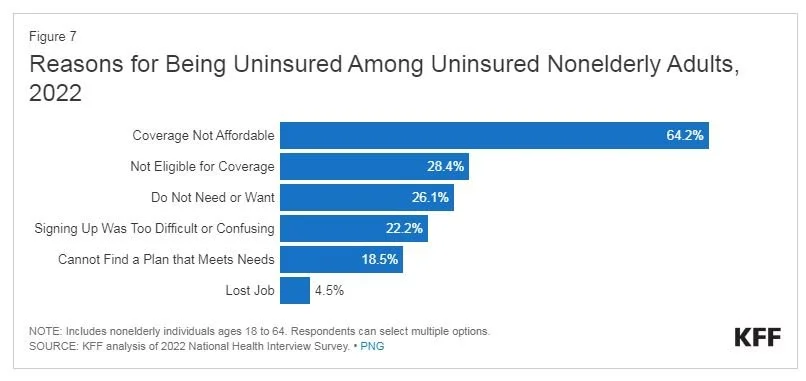

Cost still poses a major barrier to coverage for people who are uninsured. In 2022, 64.2% of uninsured nonelderly adults said they were uninsured because coverage is not affordable, making it the most common reason cited for being uninsured (Figure 8). Other reasons included not being eligible for coverage (28.4%), not needing or wanting coverage (26.1%), and signing up being too difficult (22.2%).

Not all workers have access to coverage through their job. In 2022, 60.7% of nonelderly uninsured workers worked for an employer that did not offer them health benefits.4 Among uninsured workers who are offered coverage by their employers, cost is often a barrier to taking up the offer. From 2013 to 2022, total premiums for family coverage increased by 42%, outpacing wage growth, and the worker’s share increased by 39%.5 Low-income families with employer-based coverage spend a significantly higher share of their income toward premiums and out-of-pocket medical expenses compared to those with income above 200% FPL.6 Particularly among people working for small employers, premium contributions for dependents can be unaffordable.

Medicaid eligibility varies across states and eligibility for adults is limited in states that have not expanded Medicaid. As of December 2023, 41 states including DC had adopted the ACA Medicaid expansion, although only 39 states had implemented the expansion in 2022.7 In states that have not expanded Medicaid, the median eligibility level for parents is just 37% FPL and adults without dependent children are ineligible in most cases. Additionally, in non-expansion states, millions of poor uninsured adults fall into a “coverage gap” because they earn too much to qualify for Medicaid but not enough to qualify for Marketplace premium tax credits.

Many lawfully present immigrants must meet a five-year waiting period after receiving qualified immigration status before they can qualify for Medicaid. States have the option to cover eligible children and pregnant people without a waiting period, and as of January 2023, 35 states have elected the option for children and 26 states have taken up the option for lawfully present pregnant individuals. Lawfully present immigrants are eligible for Marketplace tax credits, including those who are not eligible for Medicaid because they have not met the five-year waiting period. However, undocumented immigrants are ineligible for federally funded coverage, including Medicaid or Marketplace coverage.8 Some states have taken steps to provide fully state-funded coverage to some groups of immigrants who remain eligible for federal coverage.

Though financial assistance is available to many of the remaining uninsured under the ACA, not everyone who is uninsured is eligible for free or subsidized coverage. Six in ten (15.3 million) uninsured individuals in 2022 were eligible for financial assistance either through Medicaid or through subsidized Marketplace coverage (Figure 8). However, four in ten uninsured (10.3 million) are outside the reach of the ACA because their state did not expand Medicaid, their immigration status made them ineligible, or they were deemed to have access to an affordable Marketplace plan or offer of employer coverage. Some uninsured who are eligible for help may not be aware of coverage options or may face barriers to enrollment, and even with enhanced subsidies, Marketplace coverage may be unaffordable for some uninsured individuals

How does not having coverage affect health care access?

Health insurance makes a difference in whether and when people get necessary medical care, where they get their care, and ultimately, how healthy they are. While the COVID-19 pandemic affected health care utilization broadly, uninsured adults are far more likely than those with insurance to postpone health care or forgo it altogether because of concerns over costs. The consequences can be severe, particularly when preventable conditions or chronic diseases go undetected.

Key Details:

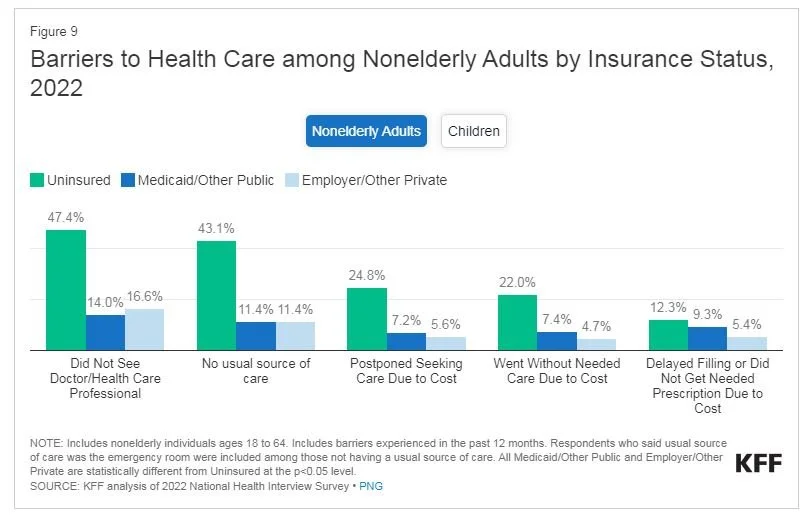

Studies repeatedly demonstrate that uninsured individuals are less likely than those with insurance to receive preventive care and services for major health conditions and chronic diseases.9, 10, 11, 12 Although overall utilization of health care services declined during the pandemic, uninsured adults were more likely to report cost barriers than barriers due to COVID-19 as the reason for delaying or forgoing care in 2021. In 2022, nearly half (47.4%) of nonelderly uninsured adults reported not seeing a doctor or health care professional in the past 12 months compared to 16.6% with private insurance and 14.0% with public coverage. Part of the reason for not accessing care among uninsured individuals is that many (43.1%) do not have a regular place to go when they are sick or need medical advice (Figure 9). But cost also plays a role. Over one in five (22.0%) nonelderly adults without coverage said that they went without needed care in the past year because of cost compared to 4.7% of adults with private coverage and 7.4% of adults with public coverage. A KFF survey that asks about cost barriers for individuals and their family members reports higher percentages of both uninsured and insured people delaying or forgoing needed due to cost.

Many uninsured people do not obtain the treatments their health care providers recommend for them because of the cost of care. In 2022, uninsured nonelderly adults were over twice as likely as adults with private coverage to say that they delayed filling or did not get a needed prescription drug due to cost (12.3% vs. 5.4%). And while insured and uninsured people who are injured or newly diagnosed with a chronic condition receive similar plans for follow-up care, people without health coverage are less likely than those with coverage to obtain all the recommended services.13, 14

Uninsured children were more likely than those with private insurance to go without needed care due to cost in 2022 (8.6% versus less than 1%). Furthermore, nearly one-quarter (24.5%) of uninsured children had not seen a doctor in the past year compared to 4.3% and 5.7% for children with public and private coverage, respectively (Figure 9).

Because people without health coverage are less likely than those with insurance to have regular outpatient care, they are more likely to be hospitalized for avoidable health problems and to experience declines in their overall health. When they are hospitalized, uninsured people receive fewer diagnostic and therapeutic services and also have higher mortality rates than those with insurance.15, 16, 17, 18, 19

Research demonstrates that gaining health insurance improves access to health care considerably and diminishes the adverse effects of having been uninsured. A review of research on the effects of the ACA Medicaid expansion finds that expansion led to positive effects on access to care, utilization of services, the affordability of care, and financial security among the low-income population. Medicaid expansion is associated with increased early-stage diagnosis rates for cancer, lower rates of cardiovascular mortality, and increased odds of tobacco cessation.20, 21,22

Public hospitals, community clinics and health centers, and local providers that serve underserved communities provide a crucial health care safety net for uninsured people. However, safety net providers have limited resources and service capacity, and not all uninsured people have geographic access to a safety net provider.23, 24, 25 High uninsured rates contribute to rural hospital closures and greater financial challenges for rural hospitals, leaving individuals living in rural areas at an even greater disadvantage to accessing care.26, 27 Research indicates that Medicaid expansion is associated with reductions in uncompensated care costs and improved financial performance for rural hospitals and other providers.

What are the financial implications of being uninsured?

Uninsured individuals often face unaffordable medical bills when they do seek care. These bills can quickly translate into medical debt since most people who are uninsured have low or moderate incomes and have little, if any, savings.

Key Details:

Those without insurance for an entire calendar year pay for almost 40% of their care out-of-pocket.28 In addition, hospitals frequently charge uninsured patients higher rates than those paid by private health insurers and public programs.29, 30, 31, 32

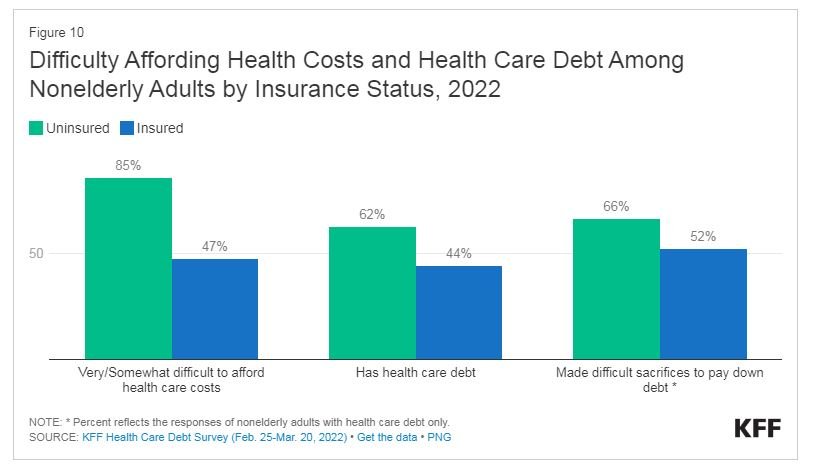

Uninsured nonelderly adults are much more likely than their insured counterparts to lack confidence in their ability to afford usual medical costs. Over eight in ten (85%) of uninsured nonelderly adults say they have difficulty affording health care costs, compared to 47% of adults with insurance (Figure 10).

Unaffordable medical bills can lead to medical debt, particularly for uninsured adults. More than six in ten (62%) uninsured adults report having health care debt compared to over four in ten (44%) insured adults (Figure 10). Uninsured adults are more likely to face negative consequences due to health care debt, such as using up savings, having difficulty paying other living expenses, or borrowing money.33 34 35 Beyond the significant financial consequences of having debt, two-thirds of uninsured adults with health care debt say they have had to make difficult sacrifices, such as eating less, changing their housing situation, or increasing work hours to pay down their debt.

While federal and state laws require certain hospitals to provide some level of charity care, not all eligible patients benefit from these programs. Consequently, charity care costs represent a small share of operating expenses at many hospitals.

Research suggests that gaining health coverage improves the affordability of care and financial security among the low-income population. Multiple studies of the ACA found declines in trouble paying medical bills and reductions in medical debt in expansion states relative to non-expansion states. More recent research found that Medicaid expansion decreased catastrophic health expenditures and was associated with greater increases in income among low-income individuals.

Conclusion

During the third year following the start of the pandemic, the number of people without health insurance continued to drop, reaching an all-time low in 2022. With pandemic-related coverage protections still in place and a strong job market, the coverage gains were driven by increases in employer, Medicaid, and non-group coverage for nonelderly adults. While the improvements in coverage were widespread, they were particularly large for American Indian and Alaska Native and Hispanic people (although these groups remain more likely than White people to be uninsured), those in low-income families, particularly people in poverty, and among people in working families, including those with only part-time workers in the family.

The end of the Medicaid continuous enrollment provision is likely to reverse these recent coverage gains. States resumed Medicaid redeterminations in April 2023 and are disenrolling people who are no longer eligible or who are unable to complete the renewal process even if they remain eligible. Net Medicaid enrollment declined by nearly three million people from March to July 2023. While some people who are losing Medicaid are gaining other coverage through an employer or through the Marketplace, some are undoubtedly becoming uninsured. Efforts by states, providers, health plans, and others to increase outreach, and the availability of Navigators and enrollment assisters to help people complete the Medicaid renewal process can increase the likelihood that eligible individuals retain Medicaid and those who are no longer eligible obtain other coverage. The extension of the enhanced Marketplace subsidies will make that coverage more affordable for people who are disenrolled from Medicaid and may increase the share of people who successfully transition from Medicaid to Marketplace coverage. Still, any large increase in the number of people who are uninsured could undermine improvements in access to care and financial stability that come with having health coverage and could worsen disparities in health outcomes.